The oil and gas industry keeps Texas running — and it operates in one of the most hazardous environments in American business. Heavy equipment, flammable materials, high-pressure systems, and remote worksites demand serious, industry-specific insurance protection.

Many oil and gas business owners — especially smaller independents and contractors — underestimate the complexity of their insurance needs. They may carry a general liability policy and assume that is sufficient, or rely on coverage requirements set by larger operators without fully understanding what those requirements actually cover.

The reality is that a single incident — whether a blowout, an equipment fire, a vehicle accident on a lease road, or a worker injury — can produce losses that quickly run into six or seven figures. This guide covers the most important coverages, the risks that drive those needs, and a real-world example of what happens when coverage gaps are exposed at the worst possible time.

Understanding the Risk

Why Oil & Gas Businesses Face Extraordinary Risk

Oil and gas operations expose businesses to risks that most industries never encounter. Working with combustible and pressurized substances means accidents can escalate rapidly. Worksites are often remote, delaying emergency response and increasing the severity of incidents. Third-party contractors and vendors create complex liability webs. Environmental regulations add another layer — a spill or release can trigger costly cleanup obligations and regulatory penalties.

Infographic · Part A

Risk Landscape

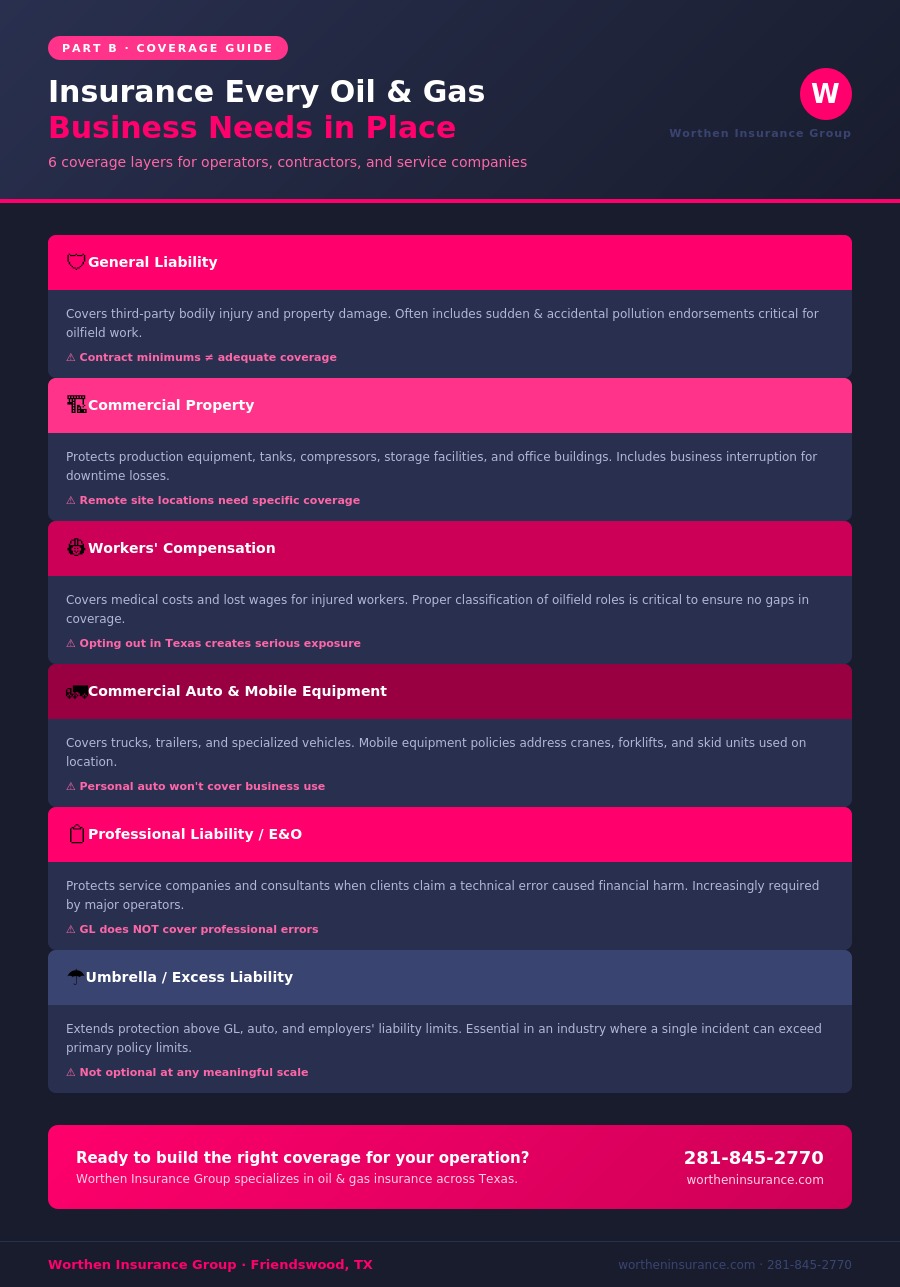

General Liability Insurance

General liability is the baseline coverage for any oil and gas business. It protects against third-party claims of bodily injury and property damage arising from your operations. If a visitor is injured at your facility, your equipment damages a landowner’s property, or your operations cause harm to a neighboring business, general liability responds.

For oil and gas companies, general liability policies often include endorsements specific to the industry, such as sudden and accidental pollution coverage, which addresses environmental releases that occur unexpectedly during operations.

Oil and gas operators working with larger companies are typically required to carry minimum liability limits specified in their contracts. However, meeting a contract requirement is not the same as being adequately covered.

Commercial Property Insurance

Oil and gas businesses often own or operate significant physical assets — production equipment, tanks, compressors, wellheads, storage facilities, and office buildings. Commercial property insurance protects these assets against fire, windstorm, hail, explosion, vandalism, and theft.

Standard commercial property policies may exclude or limit coverage for equipment located in remote or hazardous locations. Working with an agent who understands the industry ensures your policy covers the assets you actually have and where they are deployed.

Equipment breakdown coverage is another component worth discussing. When mechanical or electrical failure causes a breakdown, this coverage can step in to cover the repair costs and income lost during downtime.

Workers’ Compensation Insurance

The oil and gas industry consistently ranks among the most dangerous in the United States for workplace injuries and fatalities. Drilling, completion, production, and pipeline work all carry significant injury risk.

Workers’ compensation covers medical expenses and a portion of lost wages for employees injured on the job, and it provides an important liability shield that limits your exposure to civil lawsuits from injured workers. For oil and gas businesses, opting out in Texas is rarely advisable given the elevated risk.

Securing appropriate workers’ compensation for oilfield employees can be more complex than for standard businesses, as classification codes and experience modifiers significantly affect premium.

Commercial Auto & Mobile Equipment Coverage

Transportation is central to oil and gas operations. Trucks, trailers, frac tanks, vacuum trucks, and specialized vehicles move constantly between worksites, facilities, and supply yards. Commercial auto insurance covers these vehicles and is essential for any business operating a fleet.

Beyond standard commercial auto, oil and gas businesses often need coverage for mobile equipment that does not travel on public roads — cranes, forklifts, skid units, and other equipment used on location.

Hired and non-owned auto coverage is also worth considering for businesses where employees occasionally drive personal or rented vehicles on company business.

Professional Liability / Contractor’s E&O

Oil and gas service companies, consultants, engineers, and inspection firms carry professional liability exposure that general liability does not address. If your company provides technical services or advice and a client claims your work caused financial harm, professional liability coverage responds to those claims.

For oilfield service contractors, errors in well design, completion work, measurement, or inspection can result in significant downstream losses for the operator. This coverage is increasingly required by larger operators when contracting with service companies.

Umbrella and Excess Liability

Oil and gas service companies, consultants, engineers, and inspection firms carry professional liability exposure that general liability does not address. If your company provides technical services or advice and a client claims your work caused financial harm, professional liability coverage responds to those claims.

For oilfield service contractors, errors in well design, completion work, measurement, or inspection can result in significant downstream losses for the operator. This coverage is increasingly required by larger operators when contracting with service companies.

Infographic · Part B

Coverage Guide

Real-World Scenario

Why Oil & Gas Businesses Face Extraordinary Risk

Oil and gas operations expose businesses to risks that most industries never encounter. Working with combustible and pressurized substances means accidents can escalate rapidly. Worksites are often remote, delaying emergency response and increasing the severity of incidents. Third-party contractors and vendors create complex liability webs. Environmental regulations add another layer — a spill or release can trigger costly cleanup obligations and regulatory penalties.

Built for Risk, Protected for the Long Run

Oil and gas businesses take on significant risk every day to do work that matters. The right insurance program does not eliminate that risk, but it ensures that a single incident does not become a business-ending event.

From general liability and workers’ compensation to commercial auto, professional liability, and umbrella coverage, every layer of protection plays a role in keeping your operation financially stable when the unexpected happens.

The question every oil and gas business owner should be asking is this: if something went wrong on a job site tomorrow, would your current coverage be enough to protect your business, your employees, and your financial future?

Ready to Build the Right Coverage for Your Operation?

Worthen Insurance Group serves oil and gas operators, contractors, and service companies across Texas with customized insurance solutions built for the industry.