How to Choose the Right Cyber Insurance Policy

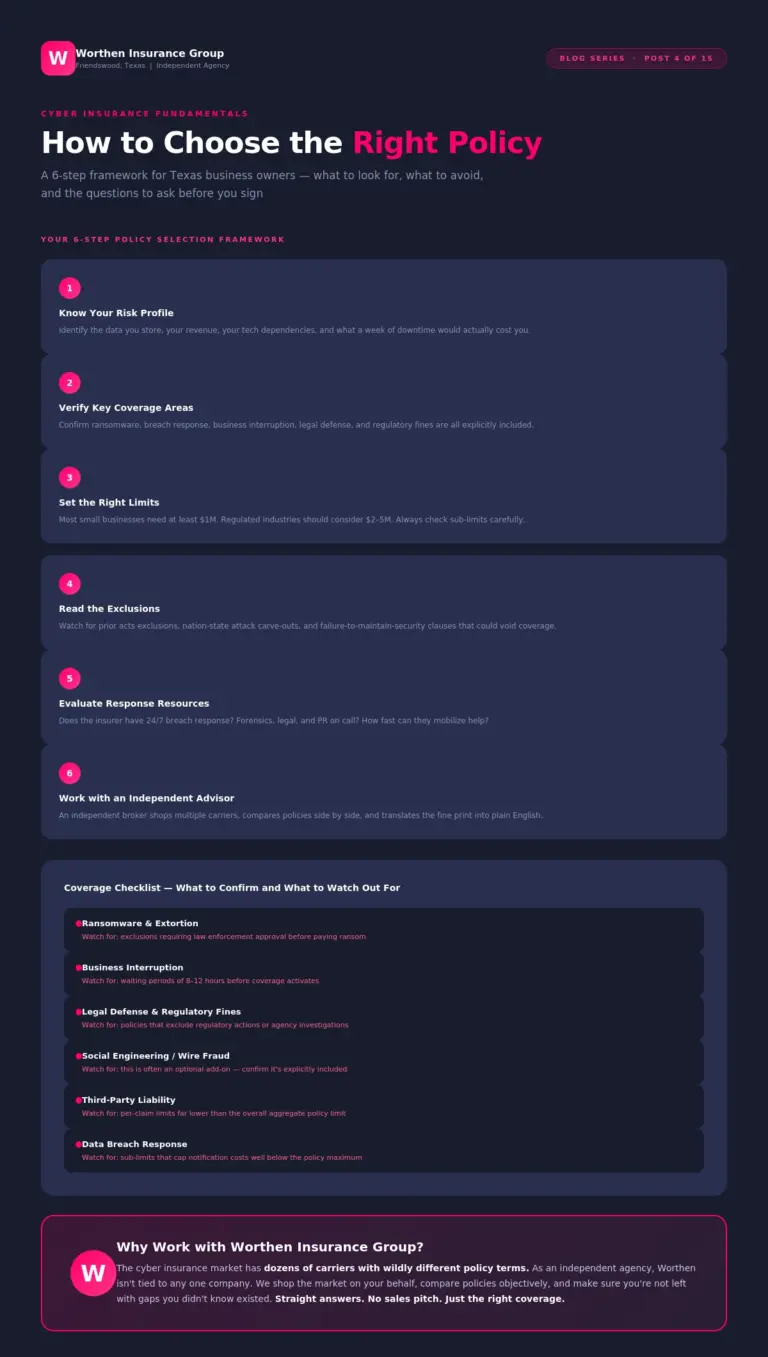

Choosing cyber insurance isn’t about grabbing the cheapest premium. It’s about matching coverage to the way your business actually operates and where you’re exposed. This post walks through a practical 6-step framework: start by sizing up your risk profile (data volume, vendors, downtime impact, and contract requirements), then confirm the “must-have” coverages like ransomware/extortion, breach response, business interruption, legal defense, regulatory fines, and social engineering. It also explains the fine print that trips companies up most, including sub-limits, waiting periods, and common exclusions like failure to maintain security or nation-state/war wording, so you can set limits that won’t come up short when it matters.