What Does Cyber Insurance Actually Cost?

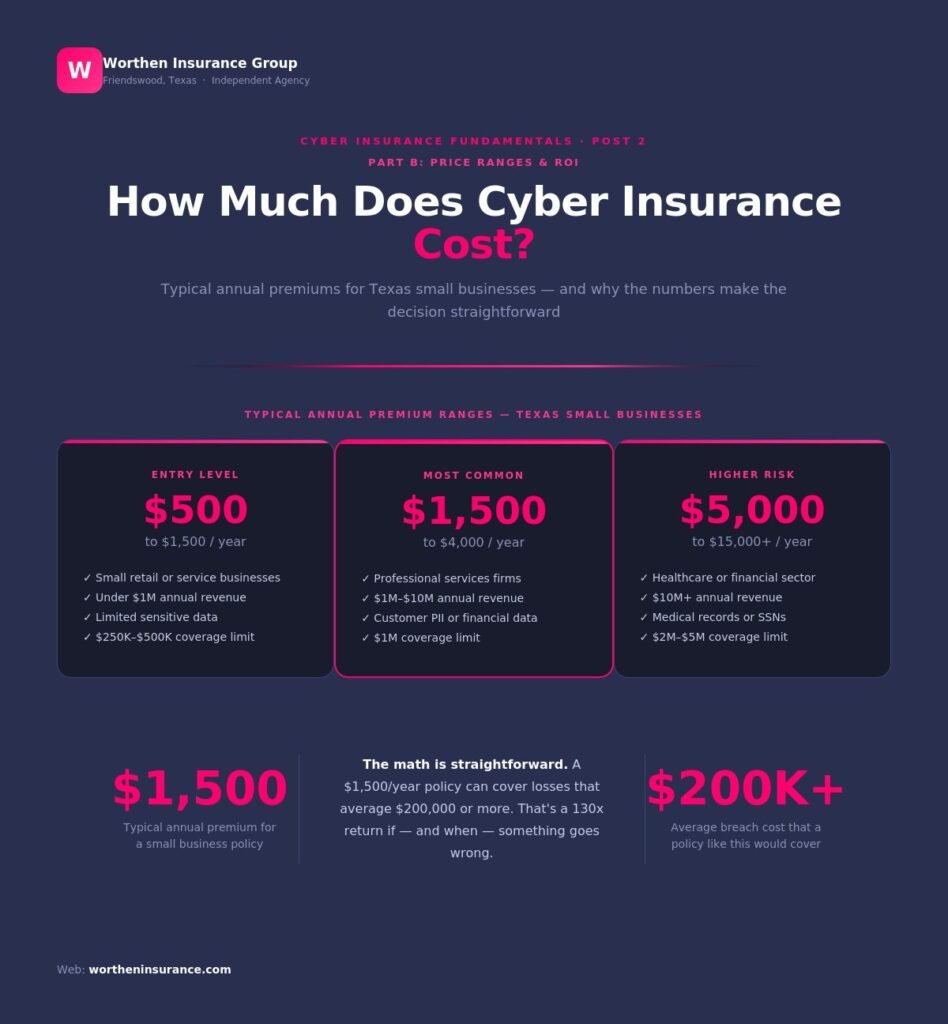

For most small and mid-size businesses, premiums fall between $500 and $5,000 per year — with the typical small business paying around $1,500 annually, or about $125 a month.

The table below shows typical ranges based on business size:

| Business Size | Typical Annual Cost | Monthly Estimate |

|---|---|---|

| Micro (1–10 employees) | $500 – $1,500/yr | ~$40 – $125/mo |

| Small (11–50 employees) | $1,000 – $3,000/yr | ~$85 – $250/mo |

| Mid-size (51–200 employees) | $2,500 – $7,500/yr | ~$210 – $625/mo |

| High-risk industry (any size) | $3,000 – $10,000+/yr | ~$250 – $835+/mo |

These are industry averages. Your actual premium depends on the risk factors covered in the next section.

7 Factors That Determine Your Premium

Insurers evaluate a specific set of risk variables to estimate how likely you are to file a claim and how large that claim could be:

1. Industry

Healthcare, finance, and legal businesses pay more because of sensitive data and tighter regulations. Retail and food service generally pay less.

2. Annual revenue

More revenue typically means more transactions, more data, and higher exposure — which means a higher premium.

3. Volume of customer data

The more personal or financial records you store, the bigger the potential breach — and the higher your rate.

4. Security measures in place

Businesses with MFA, encrypted backups, and employee training are seen as lower risk and often pay meaningfully less.

5. Claims history

A clean history works in your favor. Prior cyber claims can significantly increase your renewal premium.

6. Coverage limits and deductibles

Higher limits cost more. A higher deductible can reduce your premium but increases your out-of-pocket expense when a claim occurs.

7. Third-party vendors

Heavy reliance on outside software, cloud platforms, or managed IT providers adds to your risk profile.

How to Lower Your Premium Before You Apply

Many businesses discover they can reduce their premium by implementing basic security measures before applying for coverage:

- Enable multi-factor authentication (MFA) on all accounts — this is the single biggest premium reducer

- Back up data regularly and store copies offsite or in the cloud

- Train employees to recognize phishing emails and suspicious links

- Keep software, operating systems, and plugins up to date

- Limit access to sensitive data — not every employee needs access to everything

- Have a written incident response plan, even a basic one

Even implementing two or three of these measures can make a visible difference in your rate.

The Bottom-Line Comparison

A $1,500 annual premium protects against losses that regularly exceed $200,000. The average ransomware recovery cost — including downtime — is $1.4 million. For the overwhelming majority of small businesses, cyber insurance is one of the most cost-effective risk decisions they can make.

Get an Accurate Quote for Your Business

The best way to know your actual cost is to get a quote tailored to your specific business. Worthen Insurance Group works with multiple top-rated carriers and will show you your options side by side — with no pressure and no jargon.

Up next in this series: Is Cyber Insurance Worth It for Small Businesses?