Manufacturing businesses invest heavily in equipment, people, processes, and relationships. A single machine breakdown, a worker injury, or a product liability claim can threaten everything — and the right insurance program is what separates a recoverable setback from a business-ending event.

Many manufacturers — especially smaller and mid-sized operations — carry basic coverage but haven’t reviewed it in years or don’t fully understand what it does and does not cover. Standard policies often have critical gaps around products liability, equipment breakdown, and business interruption.

This guide breaks down the key insurance coverages every manufacturer should have, the risks behind each, and a real-world scenario that shows what happens when gaps in coverage are discovered after an incident occurs.

Understanding the Risk

Three Major Risk Categories Every Manufacturer Faces

Manufacturing risk falls into three distinct categories: physical asset risk (your plant, equipment, and inventory), workforce injury risk (one of the highest-injury industries in the U.S.), and products liability risk (once your product leaves the facility, you still bear responsibility if it fails). Understanding all three is essential to building a complete insurance program.

Infographic · Part A

Risk Landscape

What Manufacturers Risk

Every Day on the Floor

The three major risk categories — and the everyday exposures beneath them

RISK CATEGORY 1

Physical Asset Risk

Your plant, equipment, raw materials, and inventory are significant assets. Fire, storm, equipment failure, and theft can halt production and cause major losses.

RISK CATEGORY 2

Workforce Injury Risk

Manufacturing is one of the most injury-prone industries in the U.S. Lacerations, crush injuries, chemical exposure, repetitive strain, and falls are all common claims.

RISK CATEGORY 3

Products Liability Risk

Once your product leaves the facility, you still bear responsibility. A defective or improperly labeled product can trigger lawsuits that trace directly back to your operation.

EVERYDAY EXPOSURES INSIDE EACH CATEGORY

Fire & Equipment Breakdown

Industrial machinery fails unexpectedly. A motor burnout or conveyor failure can halt production for days or weeks.

Electrical & Mechanical Failure

Standard property policies don’t cover equipment that breaks from within. Equipment breakdown coverage fills this gap.

Machinery & Press Injuries

Operating presses, lathes, and cutting equipment creates daily injury exposure. Workers’ comp claims in manufacturing are frequent and costly.

Supplier Component Defects

A defective part sourced from a vendor can still create liability for your finished product — even if you didn’t manufacture the faulty component.

#4

Manufacturing ranks 4th in U.S. industries for nonfatal workplace injuries per year

$1.1M

Combined products liability claim from a defective gasket batch — real Texas case

Days

Even a brief production halt from fire or equipment failure can cascade into weeks of lost revenue

Worthen Insurance Group · Friendswood, TX

wortheninsurance.com · 281-845-2770

General Liability + Products Liability

General liability insurance is the foundation of a manufacturer’s risk program. It covers third-party bodily injury and property damage claims arising from your operations, premises, and — critically — your products. Products liability protects your business when a product you manufactured causes injury or property damage after it has left your control.

A defective component, an improperly labeled product, a batch that does not meet specifications, or a product that fails under normal use conditions can all trigger claims. Even if your manufacturing process is sound, defending a products liability claim without insurance coverage can be financially devastating.

General liability also covers premises liability — protecting you if a vendor, customer, delivery driver, or visitor is injured at your facility.

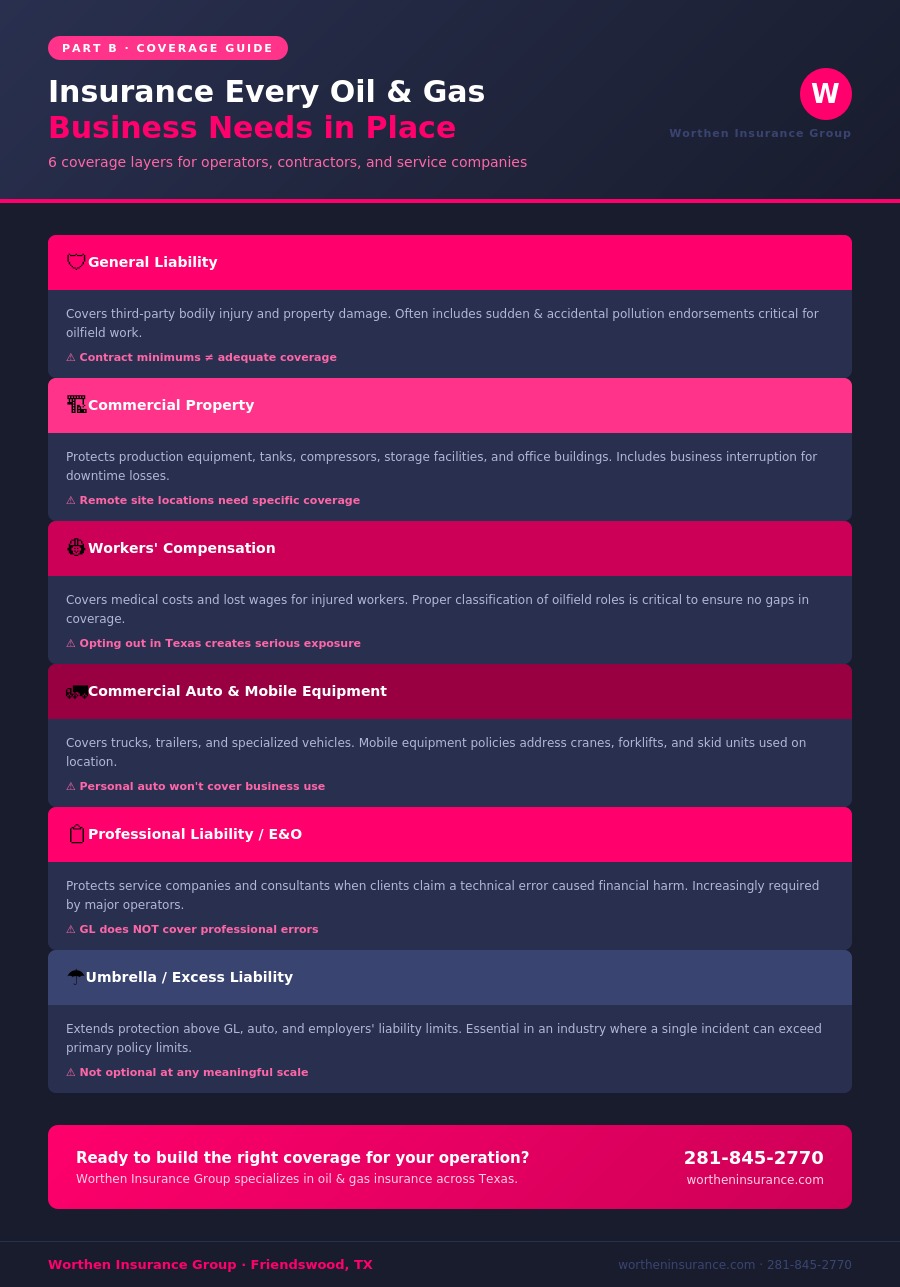

Commercial Property Insurance

Oil and gas businesses often own or operate significant physical assets — production equipment, tanks, compressors, wellheads, storage facilities, and office buildings. Commercial property insurance protects these assets against fire, windstorm, hail, explosion, vandalism, and theft.

Standard commercial property policies may exclude or limit coverage for equipment located in remote or hazardous locations. Working with an agent who understands the industry ensures your policy covers the assets you actually have and where they are deployed.

Equipment breakdown coverage is another component worth discussing. When mechanical or electrical failure causes a breakdown, this coverage can step in to cover the repair costs and income lost during downtime.

Workers’ Compensation Insurance

The oil and gas industry consistently ranks among the most dangerous in the United States for workplace injuries and fatalities. Drilling, completion, production, and pipeline work all carry significant injury risk.

Workers’ compensation covers medical expenses and a portion of lost wages for employees injured on the job, and it provides an important liability shield that limits your exposure to civil lawsuits from injured workers. For oil and gas businesses, opting out in Texas is rarely advisable given the elevated risk.

Securing appropriate workers’ compensation for oilfield employees can be more complex than for standard businesses, as classification codes and experience modifiers significantly affect premium.

Commercial Auto & Mobile Equipment Coverage

Transportation is central to oil and gas operations. Trucks, trailers, frac tanks, vacuum trucks, and specialized vehicles move constantly between worksites, facilities, and supply yards. Commercial auto insurance covers these vehicles and is essential for any business operating a fleet.

Beyond standard commercial auto, oil and gas businesses often need coverage for mobile equipment that does not travel on public roads — cranes, forklifts, skid units, and other equipment used on location.

Hired and non-owned auto coverage is also worth considering for businesses where employees occasionally drive personal or rented vehicles on company business.

Professional Liability / Contractor’s E&O

Oil and gas service companies, consultants, engineers, and inspection firms carry professional liability exposure that general liability does not address. If your company provides technical services or advice and a client claims your work caused financial harm, professional liability coverage responds to those claims.

For oilfield service contractors, errors in well design, completion work, measurement, or inspection can result in significant downstream losses for the operator. This coverage is increasingly required by larger operators when contracting with service companies.

Umbrella and Excess Liability

Oil and gas service companies, consultants, engineers, and inspection firms carry professional liability exposure that general liability does not address. If your company provides technical services or advice and a client claims your work caused financial harm, professional liability coverage responds to those claims.

For oilfield service contractors, errors in well design, completion work, measurement, or inspection can result in significant downstream losses for the operator. This coverage is increasingly required by larger operators when contracting with service companies.

Infographic · Part B

Coverage Guide

Real-World Scenario

Why Oil & Gas Businesses Face Extraordinary Risk

Oil and gas operations expose businesses to risks that most industries never encounter. Working with combustible and pressurized substances means accidents can escalate rapidly. Worksites are often remote, delaying emergency response and increasing the severity of incidents. Third-party contractors and vendors create complex liability webs. Environmental regulations add another layer — a spill or release can trigger costly cleanup obligations and regulatory penalties.

Built for Risk, Protected for the Long Run

Oil and gas businesses take on significant risk every day to do work that matters. The right insurance program does not eliminate that risk, but it ensures that a single incident does not become a business-ending event.

From general liability and workers’ compensation to commercial auto, professional liability, and umbrella coverage, every layer of protection plays a role in keeping your operation financially stable when the unexpected happens.

The question every oil and gas business owner should be asking is this: if something went wrong on a job site tomorrow, would your current coverage be enough to protect your business, your employees, and your financial future?

Ready to Build the Right Coverage for Your Operation?

Worthen Insurance Group serves oil and gas operators, contractors, and service companies across Texas with customized insurance solutions built for the industry.