The Most Common Objections — Answered Honestly

If you have been putting off cyber insurance, you have probably had one of these thoughts. Here is the honest response to each.

“We’re too small to be a target.”

This is the most dangerous misconception in cybersecurity. Attackers don’t primarily target businesses because they’re large — they target them because they’re vulnerable. Small businesses are easier to breach because they typically have fewer security resources and less oversight. Many automated attacks simply scan the internet for unprotected systems regardless of business size.

“We have antivirus software.”

Antivirus is a layer of defense, not a guarantee. Modern attacks — especially phishing and social engineering — exploit human behavior rather than software vulnerabilities. One employee clicking the wrong link can bypass your entire technical defense stack.

“We’ve never had an incident before.”

Past safety is a poor predictor of future cyber risk. The threat landscape changes constantly, and many businesses don’t know they’ve been breached until months after the fact — by which point significant damage has already been done.

“It’s just another expense I can’t afford.”

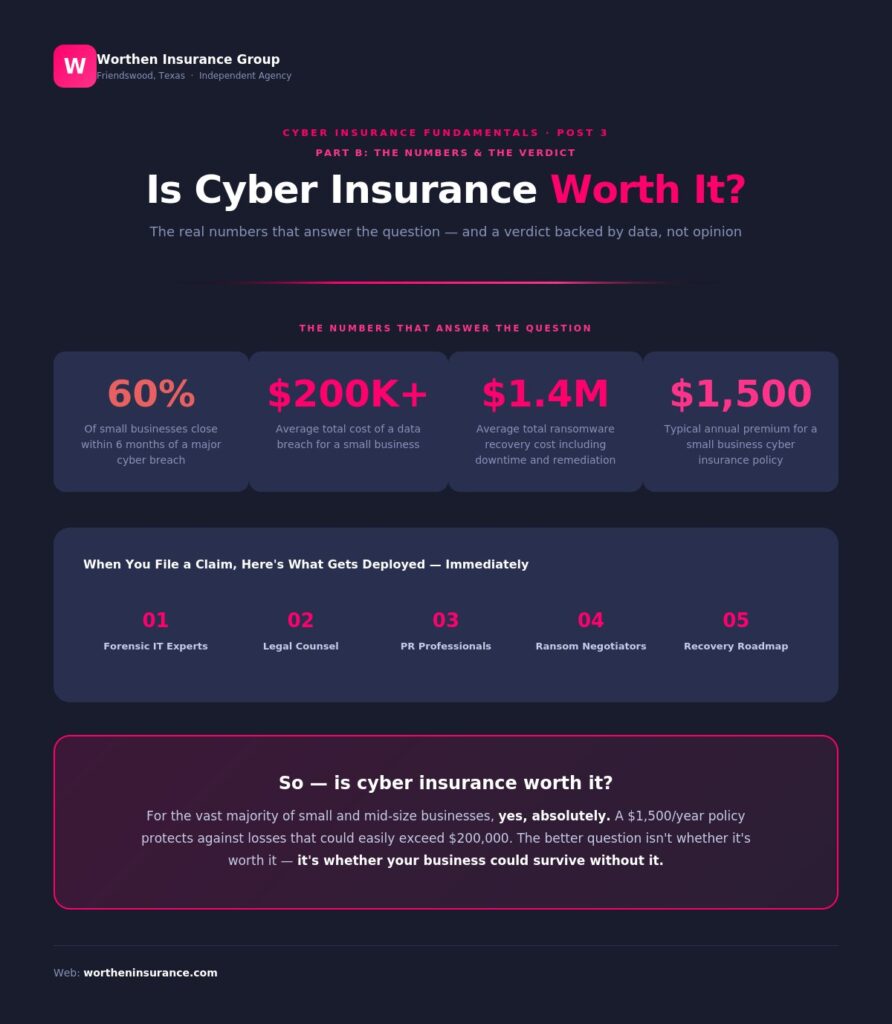

This is actually the strongest argument for getting coverage. If your business cannot comfortably absorb a $50,000–$200,000 loss, you cannot afford to go without it. Cyber insurance exists precisely for businesses that would not survive a major incident on their own.

What Happens to Businesses That Get Hit Without Coverage?

The numbers tell a sobering story:

- Customer notification and credit monitoring for a mid-sized breach: $10,000–$50,000

- 60% of small businesses that suffer a major cyberattack close within six months

- Average cost of a data breach for a small business: $200,000+

- Average ransomware recovery cost including downtime: $1.4 million

- Legal costs from a single breach lawsuit can exceed $50,000 before settlement

Without insurance, every one of those costs comes directly out of your business.

With insurance, most are covered — and you have expert help from the moment the incident is discovered.

What Cyber Insurance Actually Gives You

It is not just about money. When you file a cyber insurance claim, most policies give you immediate access to a full incident response team:

- Forensic IT experts who determine exactly how the breach happened and stop it from spreading

- Legal counsel to guide you through regulatory obligations and any resulting lawsuits

- Public relations professionals to manage communications and protect your reputation

- Negotiators who can work with ransomware attackers if payment is being considered

- A structured recovery roadmap so you are not improvising under pressure

For most small business owners, this expert support is just as valuable as the financial coverage — especially in the first 24–72 hours after an attack.

When Is Cyber Insurance Especially Worth It?

Cyber insurance delivers clear value for any business that relies on technology, but it is particularly critical if:

- You store any customer or employee personal data

- You process payments online or through a point-of-sale system

- A system outage would cost you revenue or client relationships

- You operate in a regulated industry: healthcare, finance, legal, or education

- You rely on third-party vendors, cloud software, or a managed IT provider

- Your clients require vendors to carry cyber liability coverage

The Verdict

For the vast majority of small and mid-size businesses, yes — cyber insurance is worth it. A policy that costs $1,500 a year provides financial protection, expert response support, and peace of mind against losses that regularly exceed $200,000. The real question is not whether it’s worth it. It’s whether your business could survive without it.

Talk to a Local Advisor — Straight Answers, No Jargon

Worthen Insurance Group has served Texas business owners for over 20 years. We will walk you through your real risk exposure, show you coverage options that fit your budget, and make sure you understand exactly what you’re buying.

Up next in this series: How to Choose the Right Cyber Insurance Policy for Your Business