The Two Buckets of Cyber Coverage

Cyber insurance is organized into two categories: first-party coverage (protecting your own business) and third-party coverage (protecting you when others make claims against you). Here is what each includes.

First-Party Coverage: Your Business Is Directly Hit

First-party coverage activates when a cyber incident directly impacts your operations. It is the most immediately relevant coverage for most small businesses.

Ransomware and Extortion

If attackers encrypt your files and demand payment to restore access, your policy covers the ransom, negotiation costs, and the forensic investigation to understand how the breach happened and prevent it from recurring.

Data Recovery and System Repair

After an attack, your systems need to be restored. Cyber insurance covers the IT specialists who recover your data, repair damaged systems, and rebuild what was destroyed — so you are not paying those emergency rates out of pocket.

Business Interruption Losses

Every hour your systems are down is revenue you are not collecting. Business interruption coverage compensates for lost income during the recovery period, so a cyber incident does not also become a cash flow crisis.

Crisis Management and Public Relations

When word gets out about a breach, your reputation is on the line. Many cyber policies include access to PR professionals who help manage communications, protect your brand, and maintain customer trust through the crisis.

$200K+

60%

average cost of a small business

data breach

of breached small businesses

close within 6 months

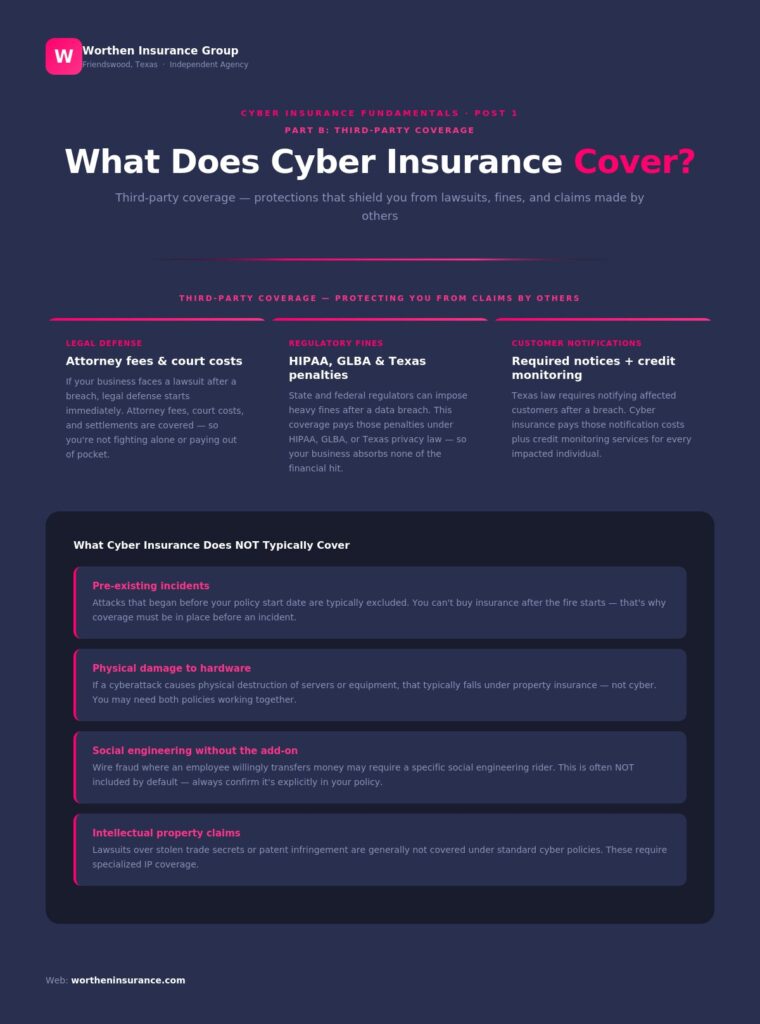

Third-Party Coverage: Protecting You from Claims by Others

If a breach exposes your customers’ or employees’ data, they may take legal action. Third-party coverage is what protects you in those scenarios.

Legal Defense Costs

Cyber insurance covers attorney fees and court costs if your business faces a lawsuit following a data breach or privacy violation. Legal defense alone can run into the tens of thousands of dollars before a single ruling is made.

Regulatory Fines and Penalties

A breach can trigger fines from state and federal regulators — particularly if you handle health data (HIPAA), financial data (GLBA), or are subject to Texas’s own data protection laws. Cyber insurance can cover those penalties.

Customer Notification and Credit Monitoring

Texas law requires businesses to notify affected customers when their data is compromised. Your policy covers the cost of those notifications and the credit monitoring services you may be obligated to provide.

What Cyber Insurance Does NOT Cover

It is equally important to know the limits. Standard cyber policies typically exclude: future lost profits beyond the recovery period, system improvements or upgrades post-attack, intentional criminal acts by employees, and physical hardware damage (covered under property insurance). Ask your advisor whether any exclusions apply to your specific situation.

Why Small and Mid-Size Businesses Need This More Than Large Ones

Large corporations have dedicated IT security teams and financial reserves to absorb a breach. Small and mid-size businesses typically have neither. One phishing email, one compromised password, one unpatched system — that is all it takes. And without cyber insurance, your business absorbs every dollar of the fallout.

The math is straightforward: a policy that costs $1,500 a year protects against losses that regularly exceed $200,000. For most small business owners, cyber insurance is one of the highest-ROI risk management decisions they can make.

Ready to Find Out What Coverage You Need?

Worthen Insurance Group has been helping Texas businesses find the right coverage for over 20 years. We are an independent agency, which means we shop multiple carriers to find the policy that fits your business — not a one-size-fits-all product.

Up next in this series: How Much Does Cyber Insurance Cost for Small Businesses?